A week or so ago, Alvaro La Parra-Perez tweeted a link to a Rafael del Pino master conference presentation (think of this as being asked to address bigwigs by Brookings Institute or American Enterprise Institute) by John Joseph Wallis of the University of Maryland. Wallis, an economic historian, entitled his presentation “The Nature of Long-Term Economic Growth”. The presentation represents research conducted jointly with Stephen Broadberry of Oxford and Warwick Universities. An early draft is available online as “Shrink Theory: The Nature of Long Run and Short Run Economic Performance” (April 2016), but this has been supplanted by a not-yet-free NBER working paper, “Growing, Shrinking, and Long Run Economic Performance: Historical Perspectives on Economic Development” (April 2017). The research has already received a capsule summary from The Economist, under the moniker “Shrink Wrap”.

Shrink Theory is remarkable – I’m going to use the catchy title of earlier paper to refer to the research – because it claims a major new empirical finding about long run economic growth AND proposes an explanation of that finding. Fittingly, the research brings together economic historians whose approaches and specializations, until recently, have been very different. Broadberry has been eminent among the company of historians who have labored to enable quantitative comparative research through backward reconstruction of time series data for European countries. Wallis, both a pupil and collaborator of the late Douglass North, is from the institutional side of the discipline. He has published in such areas as corruption, financial crises, and more recently on how countries move from “the natural state” into cooperative, growing economies. So, to set the stage, Broadberry’s work has been more to document, at a macro level, the differential paces and levels at which countries move from Malthusian to Smithian to modern economies; Wallis’s recent work has been more to ask what kind of institutional change makes such transitions possible.

To Grow More, Shrink Less

Let’s begin with the main empirical finding. Consider the green line in Fig 1 below, which is my graphing of Table 4 of the NBER working paper. The line represents the average rate of growth for 18 countries for four approximately 50-year periods. Virtually every study that ever attempted to discover the antecedents of growth either literally or implicitly regressed one or more potential “causes of growth” against the time series summarized by this line (or ones very much like it). The goal was to uncover empirically what might cause the green line to go higher, i.e., display a greater average rate of growth.

What Broadberry and Wallis have done is to divide the time series underlying the green line into up and down years and to analyze these distributions separately. Their finding , which seems to hold for multiple countries, multiple country panels, and multiple durations (and some of these series, thanks to the work of Broadberry and others, now run 700+ years), is that rapid growth is not what it is put up to be. In fact, bursts of rapid growth – because they pair with more frequent and more severe drops in per capita output – are correlated with periods where, overall, per capita GDP increases slowed, not accelerated. Conversely, improved per capita growth – such as we see over the 18-nation panel for the years 1950-2008 – was due to less shrinking, not faster growing.

I’m not going to explore the empirical results in detail. I’m also not going to pretend to know whether the authors’ approach is valid in any kind of econometric sense. Leaving that issue to the experts, it is instead fun to ask, what if the results are valid? How would Shrink theory lead us to think about business cycles and growth?

I would say that, if results hold up, then one overriding principle emerges: Less pain is more gain. This would have the following implications:

- First, the principle would dispose of pundit-beloved “no pain, no gain” theories of the economic cycle. I’m recalling, here, James Grant, and his The Problem with Prosperity, one of my absolute favorite wrong books, but I’m really referring to any kind of theory that holds that economic recessions are purifying, ultimately beneficial to the economy, and even good for the national character. The same fate would befall the kind of policy counsel that states recessions, whether they are good or bad, should be allowed to run their course. As the authors state, “Economic development depends on economies first dampening growth reversals and then stopping shrinking altogether.” (2017, p.12)

To the above I would add the hope that an established less pain/more gain principle would put an end to a form of glib consultspeak (often elevated into cultural criticism) that reverses the traditional meaning of words like “disruption”. Broadberry and Wallis show what disruption does – it reduces output. Whatever shaking things up does for business organizations, the proposition that disruption benefits economies turns out to have been demonstrably false for the last 700 years.

- But if recessions do not purge excesses, “less pain is more gain” does not mean that excesses don’t exist. Very rapid growth spurts may signify bubbles that will devolve into serious shrinkage. A confirmed Shrink Theory would imply that vigilant, party-spoiling central banking is a good thing.

- Finally – and this may be the most interesting theoretical aspect – Shrink Theory hints that today’s intense debates on the causes of falling rates of productivity increase may be misplaced, or at least wrong in their emphasis. The long-term compounding of productivity increases depends as much on stability as upon the good-years rate of increase. Put another way, the distinction between routine and transforming (or “creatively destructive”) innovation may be deceptive; it’s stability that give innovation its transforming power.

So, there is no denying the tortoise-over-hare tilt of Shrink Theory. At its extreme – which my description may have attained – the theory suggests that all the world’s economists and management consultants could be replaced with some characters from Aldous Huxley. Stepping back from that brink, the empirical side of Shrink Theory implies that Alfred Chandler has as much to say about the dynamics of growth than Joseph Schumpeter.

To Shrink Less, Get Impersonal

Modern economies grow more because they shrink less. But what has caused them to shrink less?

In the second halves of both the 2016 and 2017 papers, Broadberry and Wallis review a number of “proximate causes” for reduced shrinkage in modern economies and then suggest an “ultimate cause”. But first they pause to mention where the explanation, in their view, is not to be found:

Standard growth theory is not much help here, since it assumes away periods of shrinking and focuses only on the long run. In a neoclassical growth model with a production function and emphasis on accumulation and technical progress, it is difficult to see how an economy could shrink by five or ten percent a year for several years. (2017, p.13)

The comment is an odd one, since – at the limit – standard growth theory describes just the no-shrinkage, steady-as-you-go scenario that Shrink theory implies is desirable. That modern, developed economies were trending towards slow, steady-state growth – and not described by Roy Harrod’s step-on-your-shoelaces type of “dynamics” – was a central finding of “standard” growth theory. That said, and we will return to this at the end, growth theory’s goal was to see through shocks, Broadberry and Wallis seek to explain them.

The proximate causes considered, which receive a kind of “usual suspects” treatment, are:

- Structural change, which is primarily taken to mean the shift from mainly agricultural economies to those dominated by the manufacturing and service sectors;

- Technological change. “In theory, shrinking could disappear as the economy moves from technical stagnation to technological progress” (2017, p. 16);

- Demographic change, which the authors largely dismiss as a general cause, given the highly-varied response of countries in their panels to change in fertility and mortality;

- Changing incidence of warfare – the shocks to capacity and demand dished out by “the outbreak of war and the return to peace”.

I said “usual suspects” because, however much Broadberry and Wallis’ are willing to concede that the above factors could contribute to a reduction in shrinkage, their real concern is to bring institutional economics and to apply Wallis’ version of the transition from “identity rules” to “impersonal rules” to the problem of growing and shrinking.

Here, the exposition becomes difficult. The institutional sections of the 2016 and 2017 papers differ greatly, with the description of the rule sets being more complete in the earlier paper, but the description of the linkages to growing and shrinking far superior in the latter. What follows is purely my conflation, which I would have struggled to produce without referring to Wallis’ earlier “Institutions, organization, impersonality, and interests: the dynamics of institutions” (2011) and to Avner Greif’s earlier writing on impersonal exchange (2006) and the fundamental problems of exchange (2000), from which Wallis’ paper represents an interesting departure.

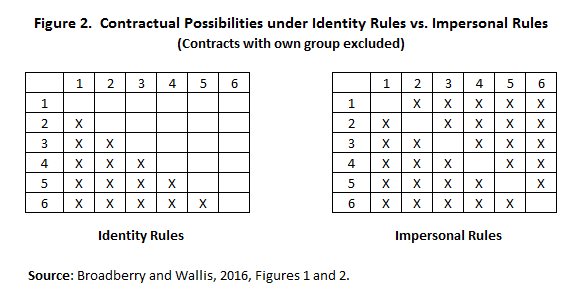

What are identity rules and impersonal rules? The latter, for this discussion, can be taken as the rule-of-law, equality-before-law combination frequently cited by institutional economists; impersonality is “treating everyone the same without regard to their individual identity” [or group affiliation] (Wallis, 2011).

But instead, let’s imagine that business contracts occur within or among members of politically ranked groups (Broadberry and Wallis call them “elites”) – with all justice dispensed in favor of the higher-ranking group. Under these “identity rules”, credible contracts can only be made within one’s group or upward (see Fig. 2). There is no way to enforce a downward obligation.

[Figure 2 goes here]

Therefore, under identity rules, the level of business activity is compressed. Fewer potential counterparties results in fewer total ventures. So, operating under identity rules, per Wallis, can mean less growth, but, and this is the key, identity rules can also mean more shrinkage – from the disruption that occurs that when elites literally fight to retain or improve their ranking. The transition from identity to impersonal rules can only occur endogenously when higher-ranking groups believe that the benefits from increased business association outweigh the advantages of rank.

Do Institutions Sanforize Economies?

The previous sections represented the two key findings of Shrink Theory. To summarize:

- Long run national income records show that increased growth depends upon reduced shrinkage, and

- The transition from identity to impersonal rules explains the reduced shrinkage that allows modern achievements in compound growth.

Note that that the second point contains the hypothesis. The first point is basically an empirical generalization – that time series of per capita growth rates have certain distributional properties, that these properties have shifted over time, and that with these shifts come the increased compounding that is seen in modern, developed economies. One may investigate this generalization or question whether it represents a valid insight, but the second point – impersonal rules cause more frequent growth and less frequent shrinkage – really is the theory.

What, then, can we say about its claim? One place to start is to ask what is missing. And one answer, clearly, would be historical particularity. Just as growth theory, through abstraction, loses track of economic oscillations, Shrink Theory, in this initial formulation and at this high level, omits the variety of institutional forms, social settings, and timings of transition that would allow us to plot the effects of institutional change – and compare those effects with those of structural change, technological change, etc. – from a specific past.

The omission is significant, I would argue, even if we agreed, somehow, that happy families are all alike and assumed a common, target institutional setup, featuring impersonal rules, for successful economies. The question remains, how did we get there? Without knowing what identity rules looked like and how they interacted with other factors (and let us add politics, geopolitics, and factor endowments to Broadberry and Wallis’ list of suspects) the term becomes, as was once said of technological change as an explanans, “a measure of our ignorance”.

But wait, you might say, this is theory, not history. And, you might add, haven’t the authors looked at multiple countries, multiple panels of countries, and multiple spans of time? Yes, they have, I would respond, they have looked at many countries, and this empirical review has provided ample grounds for a hypothesis. But they haven’t tested this hypothesis on the ground for any country – and that is the only way that this theory can be confirmed. Otherwise, there is nothing to do with this hypothesis except include an identity rules/impersonal rules switch, as a dummy variable, in yet more, future cross-country regression studies. Doing that would run into all the usual identification problems and would never establish an “ultimate cause”. No, the clincher for a theory like this will be whether, country by country, specialist historians will find it helpful in the trenches.

This said, the above as not intended as any kind of refutation, only as a reminder that there is a lot of work to do. Shrink Theory may be unconfirmed, but it is a hugely intriguing development, one that has affected my thinking even as it has triggered my usual skeptical response to broad-based institutional generalizations. Broadberry and Wallis have isolated what may be a critical principle – sustained growth requires staying out of trouble, and their application of Wallis’ identity rules framework suggests a dimension through which successful societies may have managed to get some types of disruption under control.

I want to add, as a technical note (but just a hunch, really), that as a tool for long-term historical analysis, Wallis’ identity rules may have some advantages over, say, Avner Greif’s game-theoretic comparative studies of exchange and agency arrangements. Wallis’s approach may seem less rigorous, but on the plus side it isn’t bound to exchange rules, it isn’t bound to the natural experiment of the Medieval Commercial Revolution; it isn’t crimped by the need to weigh Pareto optimality against other benefits; it may be more useful, in sum, for putting together long-term historical explanations of changing economic performance, and history, I have argued, is the court that has jurisdiction in this case. The goal, of course, is to get some Greif-ian particularity into Broadberry and Wallis’ generality.

Can Growth Theory Learn to Shrink?

As a kind of appendix, I want to return to the question of growth theory. In developing their explanation of modern reduced shrinkage, Broadberry and Wallis observed that standard growth theory is “not much help”. But could growth theory be of help – and how?

Growth theory now has multiple branches. Some of these have gone far from the standard, ratio-analysis of steady states towards approaches that make use of simulation and probabilistic outcomes (Garcia-Macia, Hsieh, and Klenow, 2016). I don’t think it is unimaginable that growth theorists could include agricultural or population shocks in their models, that they could include gradual or sudden shifts in institutional setups, or that they could model the comparative contributions of such factors, over time, for specific sets of initial conditions. Many similar things have been done in an attempt to model innovation – and that near-exclusive focus may have been exactly the problem.

But endogenous growth theory, even in its failures, may offer important lessons in how to proceed. In its attempts to convert innovation from the standard theory’s “Solow residual” into an active contributing factor, endogenous theorists repeated offered rival comprehensive theories of innovation which could satisfy no one, since innovation obviously has many entry points into the economy and takes many forms. Shrink Theory, in a search for ultimate causes, does not need to make the same mistake.

Notes

* ”Sanforized”, of course, is a garment shrinkage control technology and a trademark of GTB Holding Corporation. The Sanforization process was developed in the 1930’s by Sanford L. Cluett (1874-1968), an engineer, inventor, and (almost incidentally) a principal of the Cluett, Peabody & Co. Originally the manufacturer of Arrow shirt collars, Cluett, Peabody used the Sanforization process to achieve predictable standardization of short sizes, enabling them to launch the longtime market domination line of collar-attached Arrow shorts. Cluett, Peabody & Co. literally grew by controlling shrinkage.

References

Broadberry, Stephen, and John Wallis. “SHRINK THEORY: THE NATURE OF LONG RUN AND SHORT RUN ECONOMIC PERFORMANCE.” (2016).

Broadberry, Stephen, and John Wallis. “GROWING, SHRINKING AND LONG RUN ECONOMIC PERFORMANCE: HISTORICAL PERSPECTIVES ON ECONOMIC DEVELOPMENT.” No. 223343 National Bureau of Economic Research, 2017.

Garcia-Macia, Daniel, Chang-Tai Hsieh, and Peter J. Klenow. How Destructive is Innovation?. No. w22953. National Bureau of Economic Research, 2016.

Grant, James. The Trouble with Prosperity: The Loss of Fear, the Rise of Speculation, and the Risk to American Savings. Crown Publishing Group (NY), 1996.

Greif, Avner. “The fundamental problem of exchange: a research agenda in historical institutional analysis.” European Review of Economic History 4.03 (2000): 251-284.

Greif, Avner. “History lessons: the birth of impersonal exchange: the community responsibility system and impartial justice.” The Journal of Economic Perspectives 20.2 (2006): 221-236.

Wallis, John Joseph. “Institutions, organizations, impersonality, and interests: The dynamics of institutions.” Journal of Economic Behavior & Organization 79.1 (2011): 48-64.

Pingback: Is China making the right tradeoff between short term and long term growth? | Andrew Batson's Blog